Credit Cards: A Love Hate Relationship// Post #2: Fix Your Score

This post is part of a credit card series & I want your input!

Click the button at the end of the post to ask me all your burning credit questions.

Last week I started a series on credit cards and dove into my personal not-so-rosy history with them. Sharing my dirty laundry is cathartic, but beyond that I hope it helps my community (you!) feel better about their own personal experiences.

One of the most valuable things I did at the start of my money journey was get serious about learning. I started my career as a high school social studies teacher and when I was asked to teach my high school students a course on financial literacy in 2010, I did what any good employee would do and claimed complete confidence in my expertise on the subject. I then went home and freaked out. I knew NOTHING about financial literacy. I knew a bit about economics, but that really wasn’t the same thing. Instead of ignoring the problem as I was tempted to do, I decided that this was a sign from the universe that I needed to get my own money situation in order. I needed to school myself.

So I read. And I read. And I read. I consumed every piece of information I could find on personal finances. I read extreme blogs from people who absolutely didn’t know what they were talking about. I read super dry articles from business publications. I watched videos of screaming financial gurus (a la Suze Orman, Dave Ramsey & Jim Cramer) that just made me master the art of crawling into the fetal position.

In between the extreme and the boring, I was able to start putting together a solid foundation of financial knowledge. One of the things that fascinated me most was how credit scores were determined. Until then, I assumed that the system made sense and that I just didn’t understand it. I mean we were all buying into it, right? So how could it be wrong? I quickly discovered that the whole system was bonkers. Credit score agencies encourage people to use credit and use it frequently. The scores favor those with more accounts and those that have huge lines of credit (amount lenders are willing to give you). Paying in cash was actually going to hurt your chance of earning a badass score. The real kicker in all of this is that you need a badass score if you want to buy a home, a car, a boat or anything else that you won’t be able to pay for in cash (unless you’ve got a yacht fund you set aside for a rainy day)). It’s a total sham, y’all.

The comforting part of all of this is that once I started understanding the crazy system, I started feeling more and more confident in my own abilities to manage my money. I was slowly becoming that expert that I claimed to be from the get go! And now you can become that expert too.

Credit Scores Explained: Two Ways

Credit scores range from 300-850 and the higher you are the better. Next week we’ll dive in deeper to what those score ranges mean and how they impact our lives (getting a lease, financing a car, getting approved for a great mortgage), but today we’re going to start with breaking down how the number is determined in the first place.

1 - Credit Score Breakdown video

2 - If you don’t want to watch a video of me…

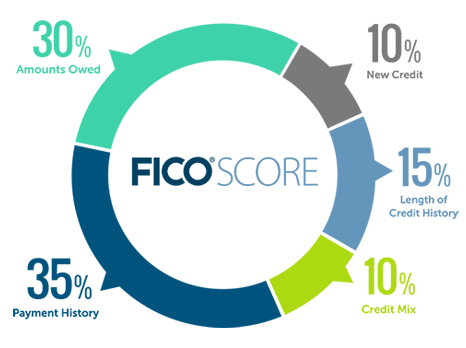

Credit Scores are determined using the following data points. Financial institutions track your history in each area and then share that information with the credit agencies (Equifax, Experian and TransUnion). I’m using the FICO breakdown in this article because that is the score that most creditors look at when assessing your credit worthiness, but for the sake of brevity I won’t go into the ins and outs of what FICO is right now.

SCORE FACTORS:

Your history with credit makes up 35% of your score

Do you pay on time? Have you ever missed a payment? Those things matter.

The more consistent you are the better!

The amount of your available credit that you use makes up 30% of your score

How much do you leave on your cards from month to month? How does that total usage compare to the amount that lenders are willing to give (i.e. your credit limits)? Are you maxed out? Maxing out hurts this part of your score!

Credit Usage = Total Balances/Total Limit

The lower your usage rate, the better (please note this is easier with larger lines of credit!)

The length of your credit history makes up 15% of your score

How long have you had your lines of credit (credit cards, car loans, student loans, mortgage, etc.)?

The longer the better! This favors older folks and people who got lines of credit at an early age.

Your credit diversity makes up 10% of your score

How many lines of credit do you have? Are there different kinds or just one?

The more diverse the better. My score actually went up when we bought a house in part because my mix got “better”

Credit checks make up 10% of your score

How many “hard checks” have you had on your credit? How many times have you applied for new cards?

The fewer checks the better

The next step is to take steps to improve the parts of the score you have control over:

Always pay off the minimum each month (need help doing this? Let’s chat!)

Call and ask your credit card companies to increase your limit (this helps your usage ratio)

Don’t close accounts (the longer you have accounts open the better, so closing accounts will hurt your “length of credit history”. There are exceptions to this rule though, so if you’re feeling unsure let me know!)

Check your score for errors (I love creditkarma.com). Checking your score isn’t a hard check so it won’t hurt your score. However, when you apply for credit or a loan they will do a hard check on you and that can hurt your score. If you find an error, it can be removed! It isn’t always a fun process, but it definitely helps your score.

If possible, don’t have any hard checks to your credit for at least 3 months. Hard checks are done by creditors to see ALL of your credit information. They have to get that information from the credit agencies I mentioned above and doing that will impact your score (ugh). Sometimes this feels like a catch-22 because you’re applying for a large line of credit! If you have questions on how to do this strategically, let me know.

Want extra tips and tricks on how to improve your score? Check out this article from Money.

Next week I’ll dive deeper into using your cards strategically.