Does it hurt your credit score to cancel cards you don’t want anymore? (This question wins for being asked the most times!)

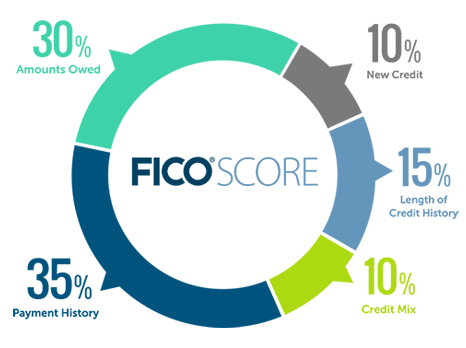

I hate this answer, but yes. A few of the factors that impact your score are hurt by closing cards: 1. Closing a card lowers the amount of credit you have available to you, making it look like you’re using more of your credit than you did before closing the card.

The math = You used to have 3 cards with the following credit limits: $5,000, $2,000 and $10,000. Your total available credit was $17,000 and you had a $2,000 balance. $2,000/$17,000 = 11% use of your cards.

Now you have 2 cards with the following credit limits: $2,000 and $10,000. Your total available credit was $12,000 and you had a $2,000 balance. $2,000/$12,000 = 17% use of your cards. Using 17% of your credit is “worse” than using 11% of it

2. Closing cards can lower your credit “diversity” and therefore lower your score.

However, hat doesn’t necessarily mean you shouldn’t close the card! There are ways to do this well, I can help.

Is it better to not have credit cards?

I know plenty of credit card-less people who are thrilled to be that way. They tend to either be independently wealthy, living off the grid, or cast members on Breaking Amish.

If you want to make big purchases that you don’t have the funds to pay for all at once (or move to a new apartment) it is really important to build a good credit score and the easiest way to do that is to use credit cards responsibly.

What is an average score?

The national average is about 700. That is a pretty good score that will get you decent loan and credit card offerings. To get the best offerings you need to score over 800, but honestly the offerings for 740+ are pretty darn close to 800+.

What is the ideal way to regularly pay off my cards?

Note: I’m answering this from the perspective of paying off your cards regularly, not if you are working on paying down balances that have been on your card for more than a month! I’ll get to that doozy next week :)

The only way to avoid interest is to make sure that your statement balance is $0 before the due date! There are a few ways to do this well. I recommend starting out with whichever option feels best for you and then checking in with yourself after a month or two. If it doesn’t actually feel good, try another option!

Pay your card balance after every purchase. This option can feel overwhelming for a lot of people, but if you’re particularly worried about getting into debt or have experienced debt in the past it just may feel right.

Pay off your balance on the same day every week. I love doing this on Fridays so you can go into the weekend feeling like a money badass!

Pay off your “statement balance” before the due date. You can either set this up as an auto pay or set up a recurring reminder for yourself to pop in and manually do it.

Is my score hurt if I get rejected for a card? What should I do next?

Sort of. Your score isn’t affected by the rejection, but it is affected by the lender doing a “hard check” on your credit history, so your score is getting hurt whether you get approved or not.

If you do get rejected, it is important to go through the following steps:

Do you need a new card right now? If not then hold off for at least 3 months while your score improves.

If you do need a new card it is important to apply for one that you are more likely to get approved for. Credit Karma has good recommendations based on your score and your bank can likely give you a good estimate of whether or not you’d be approved, but there are no sure fire bets. If you want help figuring out how to determine the right card for you, let me know!